Market Update July 2026

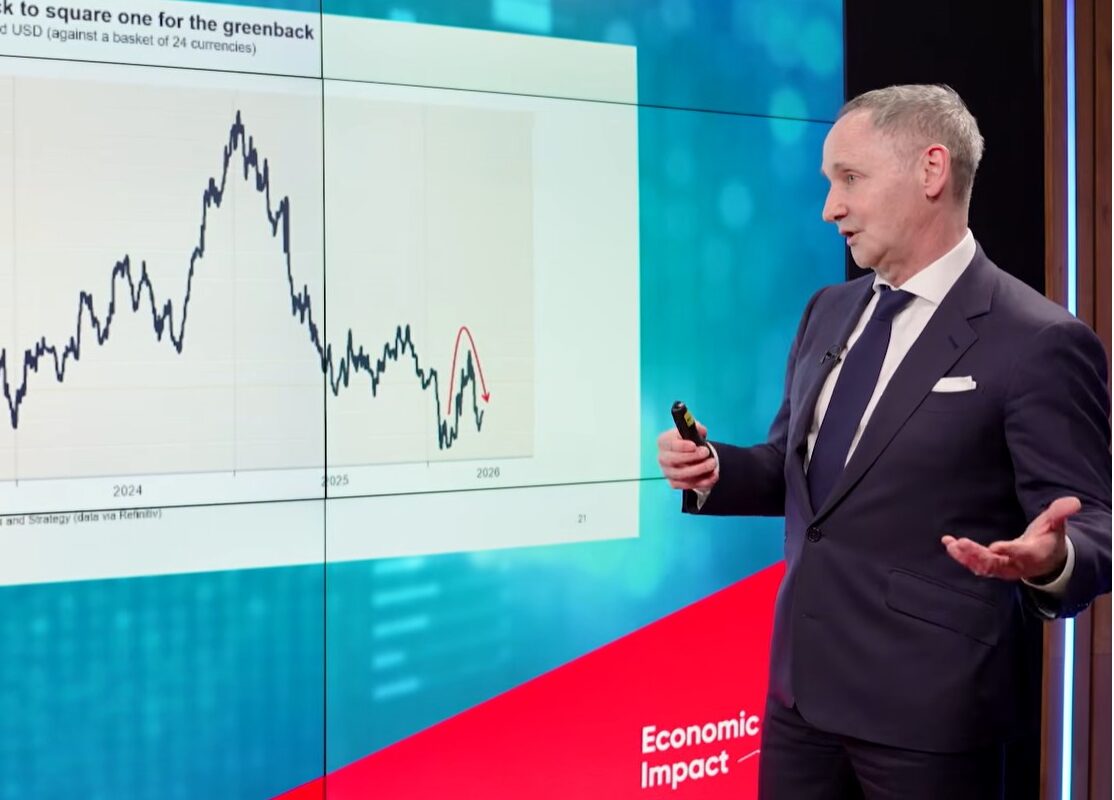

Markets have continued to advance despite a steady stream of economic and geopolitical concerns, which is a useful reminder of the old saying that “the stock market climbs a wall of worry.” In Canada, market strength has been supported primarily by the Financials, Energy, and Utilities sectors. That said, one area we are watching closely is the Canadian dollar. The currency has weakened even with firmer oil prices, reflecting broader concerns around Canada’s low productivity growth and recent softness in GDP. From a portfolio perspective, one of our key hedges against this risk remains U.S. dollar exposure within the appropriate segments of client portfolios. As part of our value proposition, we have always opened a U.S. dollar side to accounts so clients can benefit from currency, something we have found to be far less common than expected in our industry.

In the United States, market leadership remains heavily influenced by investment in artificial intelligence and related technologies. A significant share of recent S&P 500 gains has come from a relatively concentrated group of large technology companies tied to this theme. We believe exposure to this area remains important, as AI may represent the early stages of a technological shift comparable in some ways to the early days of the internet. However, position sizing and discipline matter. At some point, markets will focus more carefully on whether earnings growth is keeping pace with the substantial capital spending now being committed to AI infrastructure, and that reassessment could bring periods of volatility.

The larger question may ultimately be broader than financial markets alone. AI-driven disruption has the potential to create economic and social consequences that are more complex than a traditional market downturn. This is less about asset prices in isolation and more about how companies, workers, and economies adapt to a powerful new productivity tool. In professional settings, one of the most immediate differences may be between those who learn to use AI effectively in their daily work and those who do not. While that transition may bring disruption, we remain optimistic that it will also create meaningful opportunities as the world learns, innovates, adapts, and finds its footing.

From an investment standpoint, this is exactly why we remain disciplined. We diversify across asset classes, sectors, and geographies; emphasize quality and liquidity; rebalance portfolios proactively; and avoid reacting emotionally to headlines. Corrections, whenever they occur and whatever the catalyst, should be viewed as a normal part of investing rather than a unique event. Our approach is built on the assumption that uncertainty is constant, rather than exceptional, and portfolios should be constructed accordingly.

Periods like this, when narratives feel especially dramatic, are often when a steady, process-driven approach adds the most value. We continue to monitor earnings closely as second-quarter reporting gets underway, particularly in areas where expectations are high. At the same time, our focus remains on long-term fundamentals, risk management, and ensuring that portfolios are positioned to participate in growth while remaining resilient through inevitable periods of volatility.

As always, we would be happy to discuss these themes in more detail. They are important developments to watch, but they do not change the core principles behind the plan we have built through disciplined diversification, quality holdings, thoughtful rebalancing, and a long-term focus through changing market conditions, taking advantage of volatility through the thoughtful implementation of our covered call strategy.

We have prepared this commentary to give you our thoughts on various investment alternatives and considerations which may be relevant to your portfolio. This commentary reflects our opinions alone and may not reflect the views of National Bank Financial Group. In expressing these opinions, we bring our best judgment and professional experience from the perspective of someone who surveys a broad range of investments. Therefore, this report should be viewed as a reflection of our informed opinions rather than analyses produced by the Research Department of National Bank Financial.

Kind regards,

National Bank Financial

Rob Hunter Campbell Hunter, CIM®

Senior Wealth Advisor Wealth Advisor & Portfolio Manager

T: 250.953.8415 | F: 250.953.8470 Vancouver: 604.623.3282 |Victoria: 250.953.8422

Toll Free: 1.800.799.1175 Toll Free: 1.800.799.1175

[email protected] [email protected]

Sources: Globe and Mail, NBF Economics, The Economist

National Bank Financial – Wealth Management (NBFWM) is a division of National Bank Financial Inc. (NBF), as well as a trademark owned by National Bank of Canada (NBC) that is used under license by NBF. NBF is a member of the Canadian Investment Regulatory Organization (CIRO) and the Canadian Investor Protection Fund (CIPF), and is a wholly owned subsidiary of NBC, a public company listed on the Toronto Stock Exchange (TSX: NA).

The opinions expressed herein do not necessarily reflect those of National Bank Financial. The particulars contained herein were obtained from sources we believe to be reliable but are not guaranteed by us and may be incomplete. The opinions expressed consider a number of factors including our analysis and interpretation of these particulars, such as historical data, and are not to be construed as a solicitation or offer to buy or sell the securities mentioned herein. Unit values and returns will fluctuate, and past performance is not necessarily indicative of future performance. Important information regarding a fund may be found in the prospectus. The investor should read it before investing.

The particulars contained herein were obtained from sources we believe to be reliable but are not guaranteed by us and may be incomplete. The opinions expressed are based upon our analysis and interpretation of these particulars and are not to be construed as a solicitation or offer to buy or sell the securities mentioned herein. The opinions expressed do not necessarily reflect those of NBF.

The securities or sectors mentioned herein are not suitable for all types of investors. Please consult your Wealth Advisor to verify whether the securities or sectors suit your investor’s profile as well as to obtain complete information, including the main risk factors, regarding those securities or sectors.

We have prepared this report to the best of my judgment and professional experience to give you my thoughts on various financial aspects and considerations. The opinions expressed represent solely my informed opinions and may not reflect the views of NBF.

Selling calls against stock (Covered Writing): Shares may need to be sold at the strike price of the option at any time prior to expiration. If the calls are assigned, further opportunity for appreciation in the underlying security above the strike price is foregone.

Risk/Reward of the strategy = Strike price minus the purchase price of the underlying plus the premium received from the sale of the call. The maximum loss is the same as holding a long position less the premium received.

The investment advice given only applies to residents of the provinces of British Columbia, Alberta, Manitoba, Saskatchewan, Ontario and Quebec.

National Bank Financial is a member of the Canadian Investor Protection Fund.