Your 2025 Tax Return – Tax Reporting Information

RRSP contribution deadline for 2025 is March 2nd, 2026.

Have you made an RRSP Contribution for 2025?

- Your contribution room is limited to 18% of income earned in 2024, with a maximum contribution of $32,490 less any pension adjustments. Your 2025 limit can be found on your 2024 Notice of Assessment.

- Convenient RRSP loans are available through our affiliation with National Bank.

Have you made a TFSA Contribution for 2026?

- 2026 TFSA contribution limit is $7,000 bringing the total contribution room to $109,000*.

*Your contribution room accumulates each year in which you are 18 years of age or older and a resident of Canada, even if you do not file an income tax return or open a TFSA.

- To verify your TFSA contribution limits, please contact Canada Revenue Agency website http://www.cra-arc.gc.ca/myaccount/ or CRA directly @ 1-800-267-6999. NBF cannot be held liable for any over contribution penalties.

Income Trust or Limited Partnership Units

- Tax slips are not mailed until late March. Companies can file amendments. We suggest you wait until mid-April to file your personal tax return.

- 100% Return on Capital is recorded on the T3 and listed on the Summary of Trust Income Report.

- Reminder: If you have invested in (flow-through) Limited Partnership Units, please remember to use the tax credits applicable in future years. This is located on the final T5013 issued for any LPU. Keep copies to use these credits on your future tax returns.

- Rob suggests that clients participating in flow-through limited partnerships or options have an accountant complete their tax return. If you do not have an accountant, please feel free to contact our office for a referral.

The average U$ currency rate for 2025 is 1.3978 (applicable if you are reporting U$ capital gain/loss). Source: Bank of Canada – Financial Markets Department

Allowable capital losses can be applied against any capital gains for the previous 3 years (2022, 2023, 2024) or carried forward indefinitely.

- For clients who have taxable accounts, we will be mailing out a Capital Gain/Loss Report by Feb 15, 2026. (Please keep these reports with the rest of your tax slips to give to your accountant.)

Foreign Property Report

- Foreign Property Reports will be mailed out by Feb 15, 2026, to clients with taxable accounts that contain foreign property greater than $100,000. Please keep these reports with the rest of your tax slips to give to your accountant.

- On-line Services – if you would like to view your NBF accounts on-line, please contact me for access.

- You can now receive your monthly statements, trade confirmations and tax slips on-line too!

Your personal tax return must be filed prior to mid-night of April 30th, 2026 (post-marked or received by CRA by April 30th, 2026)

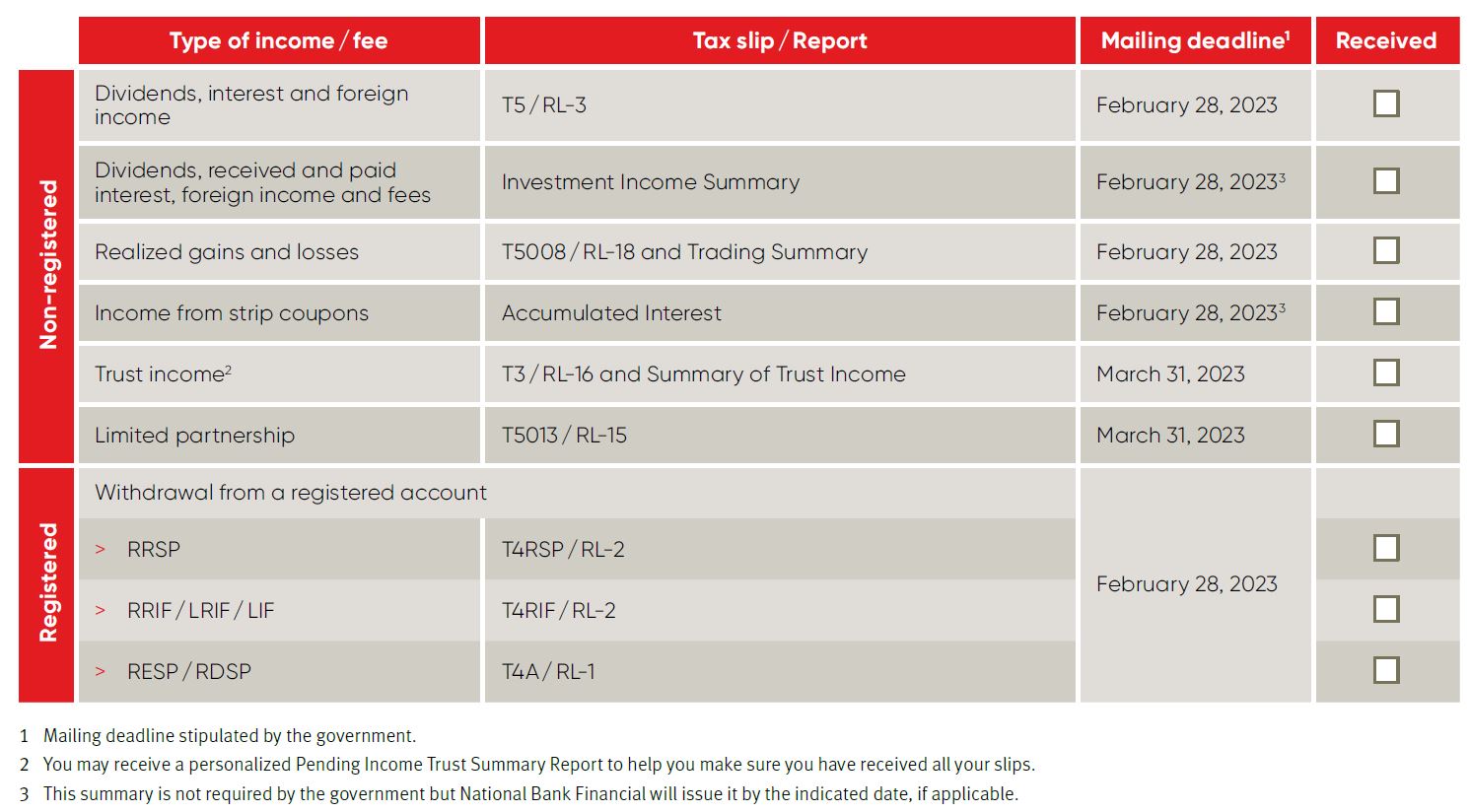

This Is When Your Tax Slips Will Be Available

This table lists the various Canadian slips and forms that may be needed to prepare your income tax return. Since these documents reflect the transactions and income recorded during the year, some may not apply to your situation. Before completing your tax return, please ensure that you have received all your tax slips to avoid having to file an amended return.

Please feel free to contact me if you have any questions or require any further information. I will be happy to be of any further assistance to you.

Comet Tang

Wealth Associate

T: 250.220.9021 | F: 250.953.8470

Toll Free: 1.800.799.1175

Email [email protected]

Website www.rhunterwealth.ca

R Hunter Wealth Management Group

National Bank Financial

Suite 700- 737 Yates Street

Victoria, BC V8W 1L6

National Bank Financial – Wealth Management (NBFWM) is a division of National Bank Financial Inc. (NBF), as well as a trademark owned by National Bank of Canada (NBC) that is used under license by NBF. NBF is a member of the Canadian Investment Regulatory Organization (CIRO) and the Canadian Investor Protection Fund (CIPF), and is a wholly-owned subsidiary of NBC, a public company listed on the Toronto Stock Exchange (TSX: NA).National Bank Financial is a member of the Canadian Investor Protection Fund (CIPF). NBF is not a tax advisor and clients should seek professional advice on tax-related matters, including their personal situation. Please note that comments included in this letter are for information purposes only and are not intended to provide legal, tax or accounting advice. The comments reflect the opinion of their author only and may not reflect the views of NBF.

NBF is not a tax advisor and clients should seek professional advice on tax-related matters, including their personal situation. Please note that comments included in this letter are for information purposes only and are not intended to provide legal, tax or accounting advice. The comments reflect the opinion of their author only and may not reflect the views of NBF.

“The securities or sectors mentioned herein are not suitable for all types of investors. Please consult your Wealth Advisor to verify whether the securities or sectors suit your investor’s profile as well as to obtain complete information, including the main risk factors, regarding those securities or sectors.”